March 24, 2026

The Strait of Hormuz Effect: The Four Main Channels of Impact on the Argentine Economy

Tensions in one of the world’s major energy corridors are already affecting freight rates, insurance, and key costs for the agricultural sector. Against this backdrop, Argentina faces an unprecedented situation: increased pressure on inputs and logistics, but also an opportunity to boost foreign exchange earnings.

Tensions in the Middle East have once again brought the Strait of Hormuz at the center of global trade. It is not just another point on the map: it is one of the main bottlenecks of the global economy.

About a quarter of the world’s maritime oil trade, as well as significant volumes of liquefied natural gas and fertilizers.

In recent days, disruptions to maritime traffic in the area led the International Maritime Organization (IMO) to convene an extraordinary session to analyze the impact on navigation and maritime safety, while UNCTAD warned that ship traffic through the strait had come to a “near standstill.”

The scale of the risk explains why the market reacted so quickly. In 2024, approximately 20 million barrels of oil per day of oil passed through the Strait of Hormuz, equivalent to more than a quarter of global maritime oil trade. In addition, nearly one-fifth of global LNG trade passed through that corridor, primarily from Qatar and the United Arab Emirates.

The transmission channel to the Argentine economy

Although Argentina does not rely directly on the Strait for grain exports, it is nonetheless affected by it in several ways.

The first is energy-related.

UNCTAD noted that, between February 27 and March 9, 2026, the price of Brent rose 27% and European natural gas 74%. At the same time, it warned that oil tanker freight rates, war risk insurance premiums, and bunker costs have been rising, driving up the cost of entire logistics chains.

The second option is fertilizers.

The World Bank notes that natural gas accounts for about 80% of the cost of urea production, so an energy shock is quickly passed on to the price of nitrogen fertilizers. And the global exposure is significant: the Rosario Stock Exchange noted that about one-third of international fertilizer trade, so a restriction in that corridor not only drives up energy costs but also the supply and CIF price of key agricultural inputs.

For Argentina, this issue is particularly sensitive. According to the Rosario Stock Exchange, by 2024 more than 65% of local fertilizer consumption was met by imports, and the country imported fertilizers worth US$1.537 billion. The BCR itself noted that urea is essential for crops such as corn and wheat—precisely two of the sectors that currently underpin a significant portion of Argentina’s export prospects.

Elevated logistics expenditures, intensifying pressure on profit margins and domestic pricing.

The third avenue involves logistics and insurance solutions.

In its assessment of the Strait of Hormuz, UNCTAD cautioned that escalating freight charges, marine bunker fuel prices, and insurance premiums could drive up expenses across the entire trade supply chain. Corroborating this, the Rosario Board of Trade estimated that the cost of shipping Argentine grains globally surged by 40% to 50%, depending on the destination, amid the ongoing escalation.

This cost escalation does not consistently translate into improved producer prices. Indeed, the BCR clarified that higher freight rates typically depress ex-farm prices, effectively anchoring FOB quotations.

Consequently, a paradox arises: while the conflict introduces a geopolitical premium to commodities, ample domestic supply and escalating logistics expenses may constrain price appreciation within Argentina.

This tension was distinctly evident in the corn market. The BCR reported that the spot price in Rosario plummeted to eight-year real lows, declining from offers of US$ 180 per tonne to values US$ 10 lower during the first week of March, driven by harvest progression and robust physical supply. Although the market subsequently rebounded to the US$ 180/t vicinity, this event underscored that domestic factors can exert greater influence than international price surges.

The Financial Factor: Funds Reallocate to Grains

The fourth avenue is financial.

Amidst geopolitical uncertainty, investment funds typically reallocate to real assets and commodities. According to the BCR, within a mere thirty trading days, speculative funds transitioned from a net short position in grains and derivatives to a net long position of 295,045 contracts, representing net purchases of approximately 540,000 contracts in Chicago. This pivot contributed to maintaining elevated international prices, particularly for wheat and soybeans.

This market dynamic holds significance for Argentina by enhancing the external economic environment, yet it does not assure a direct transmission to the domestic market. Should the conflict de-escalate, this financial positioning could rapidly reverse. Consequently, the surge in international prices may offer only partial respite and represents a fragile indicator if predicated more on financial hedging than on robust physical fundamentals.

The Argentine Paradox: External Shock Amidst Record Harvest

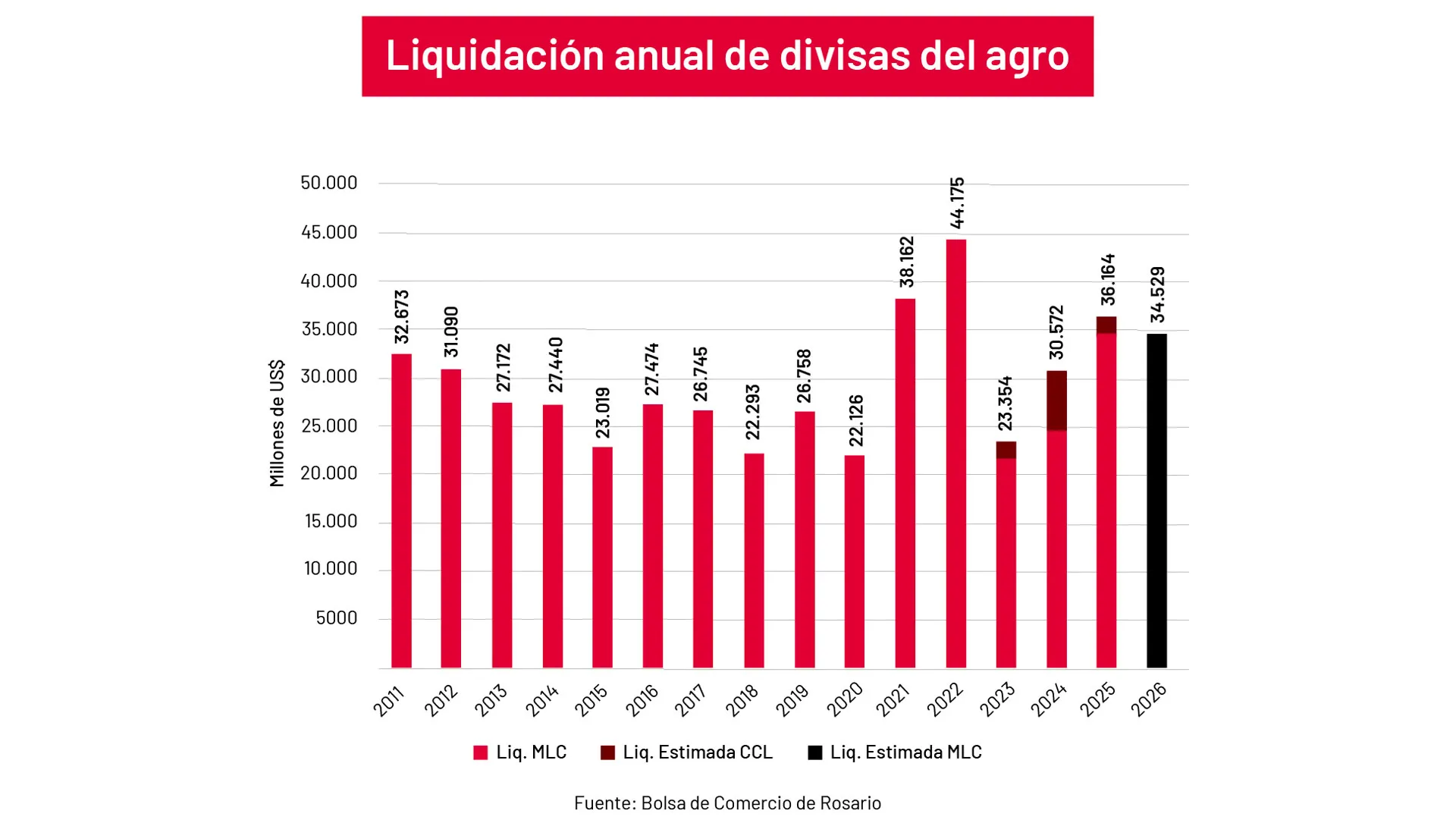

Amidst this volatility, Argentina confronts a unique scenario. The Rosario Board of Trade projects a total production of 160 million tonnes for the 2025/26 season, including a record fine grain harvest of 29.5 Mt of wheat and 5.6 Mt of barley. Furthermore, it estimates 62 Mt of corn, 6.6 Mt of sunflower and 48 Mt of soybeans. On this basis, agro-industrial exports are projected to reach US$ 34.53 billion in 2026, with export duty collection nearing US$ 4.65 billion.

From a macroeconomic standpoint, this positions the agricultural sector as a pivotal stabilizer. Should the Hormuz conflict drive up costs for energy, fertilizers, transport, and insurance, while simultaneously sustaining or enhancing international prices for grains and oils, Argentina could capitalize on a portion of this effect via its export channels.

In essence, the very shock that elevates global costs could strengthen the agricultural sector's role as a foreign exchange generator for the Argentine economy.

Potential Impacts on International Trade

Should the crisis in Hormuz persist, the repercussions would extend beyond mere price fluctuations to impact the fundamental architecture of global trade. UNCTAD cautioned that such events can rapidly propagate through energy, transportation, and agricultural inputs, imposing more severe consequences on vulnerable economies.

For international commerce, this entails at least four key consequences:

- Increased Cost Per Tonne Transported

- Heightened Exposure to War Risk Insurance

- Operational Delays

- Tactical Reallocation of Trade Flows to Alternative Routes and Suppliers.

For Argentine enterprises, this necessitates a perspective extending beyond mere commodity pricing. The inherent risks also encompass logistics, cargo insurance coverage, the volatility of financial costs, and the capacity to uphold contractual obligations within an environment characterized by fluctuating international transport premiums, transit times, and terms.

From this perspective, the conflict in Hormuz is not merely a geopolitical headline; it represents an operational risk factor for importers, exporters, logistics operators, and the entire foreign trade supply chain.

An External Crisis with Tangible Effects on Argentina

The conclusion is clear. The Strait of Hormuz may be distant, but its impact is not. Should the conflict persist, Argentina could face elevated energy costs, more expensive fertilizers, rising freight and marine insurance premiums, and increased pressure on global logistics. However, concurrently, the projected record harvest for 2025/26 and the anticipated volume of agro-industrial exports could provide the country with a crucial source of foreign currency amidst a more uncertain international landscape.

The true unknown is not merely the duration of the crisis. Equally critical is Argentina's capacity to sustain the logistical efficiency, input supply, and export competitiveness required to convert a pricing opportunity into actual foreign exchange earnings. In an increasingly volatile world, the differentiator will not solely be the harvest; it will also be the ability to manage risk.

Risk Management in an Increasingly Uncertain International Trade Environment

Within this context, risk transcends being solely productive or commercial, evolving to encompass logistical and financial dimensions. Volatility in maritime routes, escalating freight costs, and rising insurance premiums are not isolated variables; they are integral to a unified scenario where operational continuity increasingly hinges on meticulous planning.

For exporters, importers, and logistics operators, this necessitates a review not only of costs but also of coverage levels, policy scope, and actual exposure at each segment of international transit. This is particularly crucial in scenarios where route deviations, delays, or increased risks associated with geopolitically sensitive areas may arise.

Key Variables to Review for Operating in an Increasingly Uncertain Global Context:

- Review Routes and Transit Times:Assess potential deviations, conflict zones, and their impact on logistical timelines and costs.

- Analyze the Actual Exposure of Each Operation: Identify critical points at origin, in transit, and at destination where risk escalates.

- Update Contractual and Commercial Terms: Review INCOTERMS, liabilities, and clauses in anticipation of extraordinary deviations or delays.

- Validate Current Coverage and Scope: Ensure that policies account for current scenarios, including deviations, additional costs, or sensitive regions.

- Monitor Logistical and Financial Costs in Real Time: Freight, insurance, fuel, and tariffs can fluctuate rapidly during crises.

- Develop Alternative Scenarios: Anticipate contingency plans for disruptions or changes in international routes.

In this evolving global trade landscape, success is not merely about reaching the destination, but about how risks are managed throughout the journey.

To delve deeper into protecting international trade operations amidst highly volatile contexts, explore the comprehensive coverage solutions available for every cargo type and route. Contact us!

Related articles

International Freight Risk Report: 1Q2026

This report on risks in international freight transport for the first quarter of 2026 analyzes the major incidents and events that…

The Last Mile in Mexico: The Real Logistical Challenge

How last-mile logistics, parcel delivery, and shipment security directly impact the experience…

Argentina's 2026 Corn Season: Record Harvest, Rising Exports, and New Market Opportunities

With the DJVE at record highs and shipments to China, the agricultural export sector faces both opportunities and risks in the…